Northern Dynasty Receives Positive Preliminary Assessment Technical Report for Globally Significant Pebble Copper-Gold-Molybdenum Project in Southwest Alaska

February 23, 2011

Wardrop completes independent Preliminary Assessment report based on concept, pre-feasibility and feasibility-level study programs completed by Pebble Partnership and Northern Dynasty

Preliminary Assessment describes and assigns potential economic value to three mine development cases comprising 25, 45 and 78 years of open pit mining and a nominal processing rate of 200,000 tons per day

For the Pebble Project, the 45-year Reference Case yields a 14.2% pre-tax IRR, a 6.2-year payback on initial capital investment of $4.7 billion and a $6.1 billion pre-tax NPV at a 7% discount rate and long-term metal prices.

At current prevailing metal prices, the 45-year Reference Case yields a 23.2% pre-tax IRR,

a 3.2-year payback on initial capital investment and a $15.7 billion pre-tax NPV at a 7% discount rate

For Northern Dynasty’s 50% share of the project, the 45-year Reference Case yields an 18% pre-tax and 15.4% post-tax IRR, a 4.7-year pre-tax and 5.3-year post-tax payback on initial capital investment and a

$3.6 billion pre-tax and $2.4 billion post-tax NPV at a 7% discount rate and long-term metal prices.

At current prevailing metal prices, the 45-year Reference Case yields a 30.2% pre-tax and 25.1% post-tax IRR, a 2.6-year pre-tax and 3.1-year post-tax payback on initial capital investment and an

$8.3 billion pre-tax and $5.6 billion post-tax NPV at a 7% discount rate for Northern Dynasty’s 50% interest

The 45-year Reference Case produces 31 B lb copper, 30 M oz gold, 1.4 B lb molybdenum, 140 M oz silver,

1.2 M kg rhenium and 907,000 oz palladium while mining only 32% of the mineral resource

For the 45-year Reference Case, cash costs per payable lb of copper after by-product credits total –$0.11

February 23, 2011, Vancouver, BC -- A National Instrument 43-101-compliant Technical Report on a Preliminary Assessment of the Pebble Copper-Gold-Molybdenum Project (the "Pebble Project") in southwest Alaska, completed for Northern Dynasty Minerals Ltd. (TSX: NDM; NYSE Amex: NAK) by Wardrop, a Tetra Tech Company ("Wardrop"), confirms that Pebble is an economically robust project with the potential to become one of the most important metal producers of the 21st century. The Preliminary Assessment updates and substantially revises project economic analysis last done by Northern Dynasty in 2004, and so constitutes a material change for which a material change report containing the full executive summary will be shortly filed at www.sedar.com and at www.northerndynasty.com, along with a complete copy of the Technical Report.

The Preliminary Assessment is based on Wardrop's comprehensive review of recent engineering and technical studies undertaken principally by the Pebble Limited Partnership (the "Pebble Partnership") and by Northern Dynasty. The economic assessments and other opinions expressed in the Preliminary Assessment are strictly those of Northern Dynasty and Wardrop, and do not reflect the views of any other stakeholder in the project. The Pebble Partnership continues to separately undertake detailed engineering studies toward the completion of a Prefeasibility Report for the Pebble Project as contemplated by the 2007 Limited Partnership Agreement, including ongoing programs to engage project stakeholders in the planning process. As such, any project which is ultimately put forward by the Pebble Partnership for permitting under the National Environmental Policy Act (NEPA) may differ from those mine models presented in the Preliminary Assessment.

"The Pebble Project is among a handful of mineral projects around the world with the potential to meaningfully enhance global production of copper, gold and molybdenum at a time when worldwide demand is increasingly outstripping supply," said Northern Dynasty President & CEO Ron Thiessen. "After many years of exhaustive geological, environmental and socioeconomic study, as well as intensive engineering effort, this Preliminary Assessment confirms Pebble's potential as a modern, world-class mine that provides decades of benefits to shareholders, to the people and communities of Alaska, and to the U.S. and global economies."

The Preliminary Assessment describes and assigns potential economic value for three successive development cases:

- An Investment Decision Case ("IDC Case"), which describes an initial 25-year open pit mine life upon which a decision to initiate mine permitting, construction and operations may be based;

- A Reference Case, which is based on 45 years of open pit mine production; and

- A Resource Case, which is based on 78 years of open pit mine production and seeks to assess the longer-term value of the project in current dollars.

The 25-year IDC Case is the only scenario for which a tailings storage facility has been comprehensively engineered, although preliminary engineering studies have identified a number of suitable sites nearby to receive tailings after 25 years. Ongoing investigations undertaken during the first 25 years of mining, including construction of an early access shaft, would determine the optimal mining method and plan for subsequent phases of development.

For the purposes of its Preliminary Assessment, Wardrop has selected the 45-year Reference Case as its base case. All currency values are in US dollars. Production rates are stated in imperial tons.

A Preliminary Assessment is preliminary in nature, and includes Inferred mineral resources that are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no assurance that the Preliminary Assessment will be realized.

Preliminary Assessment Key Findings

- At a 0.30% CuEQ1 cutoff, the Pebble mineral resource comprises:

- 5.94 billion tonnes of Measured and Indicated resources grading 0.78% CuEQ2 , and containing 55 billion pounds of copper, 67 million ounces of gold, and 3.3 billion pounds of molybdenum; and

- 4.84 billion tonnes of Inferred resources grading 0.53% CuEQ, and containing 25.6 billion pounds of copper, 40.4 million ounces of gold, and 2.3 billion pounds of molybdenum.

- The Pebble deposit supports open pit mining utilizing conventional drill, blast and truck-haul methods, with an initial mine life of 25 years and potential for mine extensions to 78 years and beyond.

- The potential exists for underground block cave development at a mining rate of 150,000 tons per day to emerge as the preferred mining method for phases of development beyond 25 years.

- The process plant employs conventional crush-grind-float technology and equipment with a nominal throughput of 200,000 tons per day, as well as secondary gold recovery. Average mill throughput for the first 25 years would be 219,000 tons per day, rising to 229,000 tons per day for the 45-year and 78-year cases.

- Other project facilities and infrastructure include: a 378 megawatt natural gas-fired turbine plant at the mine site; an 86-mile transportation corridor to Cook Inlet for road and pipeline rights-of-way; and a new deep-water port on Cook Inlet.

- Construction of the Pebble Project would take four years, and employ a peak labour force of 2,080. The operations workforce averages 1,120 over the first 25 years of mining.

- The 45-year Reference Case processes 3.8 billion tons of material with a strip ratio of 2.1:1 and average grades of 0.46% copper, 0.011 oz gold per ton and 214 ppm molybdenum.

- The 45-year Reference Case produces 31 billion lb copper, 30 million oz gold, 1.4 billion lb molybdenum, 140 million oz silver, 1.2 million kg rhenium and 907,000 oz palladium, while mining 32% of the total Pebble mineral resource.

- Economic valuations are expressed in US dollars in real terms utilizing long-term metal prices of $2.50/lb copper, $1,050/oz gold, $13.50/lb molybdenum, $15/oz silver, $3,000/kg rhenium and $490/oz palladium.

- Annual cash flows are calculated and subsequently discounted at a rate of 7%. Market convention generally uses a discount rate of 8% for copper and other base metal projects and 5% for gold and other precious metal projects. Given the large contribution of gold to total revenues at Pebble, a 7% blended discount rate has been selected.

- For the Pebble Project, the 45-year Reference Case yields a 14.2% pre-tax Internal Rate of Return (IRR), a 6.2-year payback on initial capital investment and a $6.1 billion pre-tax Net Present Value (NPV) at long-term metal prices and a 7% discount rate. At current prevailing metal prices, the 45-year Reference Case yields a 23.2% pre-tax IRR, a 3.2-year payback on initial capital investment and a $15.7 billion pre-tax NPV at a 7% discount rate.

- For Northern Dynasty's 50% interest in the Pebble Project, the 45-year Reference Case yields an 18% pre-tax and 15.4% post-tax IRR, a 4.7-year pre-tax and 5.3-year post-tax payback on initial capital investment, and a $3.6 billion pre-tax and $2.4 billion post-tax NPV at a 7% discount rate at long-term metal prices. At current prevailing metal prices, Northern Dynasty's 50% interest in the Pebble Project yields an 30.2% pre-tax and 25.1% post-tax IRR, a 2.6-year pre-tax and 3.1-year post-tax payback on initial capital investment and an $8.3 billion pre-tax and $5.6 billion post-tax NPV at a 7% discount rate.

- Initial capital expenditures for all three development cases are estimated at $4.7 billion, excluding capital costs associated with outsourced power, road and port infrastructure. Sustaining capital requirements for the 45-year Reference Case are estimated to be $6.14 billion.

- Operating costs for the 45-year Reference Case average $966 million per year and total $43.5 billion over the life of the mine. Operating costs per ton milled average $11.55 for the 45-year Reference Case, while cash costs per payable pound of copper, after by-product credits, are -$0.11.

- Net Smelter Return (NSR) for the 45-year Reference Case averages $2.67 billion per year and totals $120.2 billion over the life of mine. NSR per ton milled for the 45-year Reference Case averages $31.91.

- For the 45-year Reference Case, 56% of NSR would be derived from copper, 24% from gold, 16% from molybdenum and 4% from other metals (silver, rhenium and palladium).

1 The Preliminary Assessment is based on mineral resources announced by Northern Dynasty in a news release dated February 1, 2010. The mineral resources fall within a volume or shell defined by long-term metal price estimates of $2.50/lb copper, $900/oz gold and $25/lb molybdenum. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Copper equivalent calculations for this resource estimate used metal prices of $1.85/lb for copper, $902/oz for gold and $12.50/lb for molybdenum, and metallurgical recoveries of 85% for copper 69.6% for gold, and 77.8% for molybdenum in the Pebble West area and 89.3% for copper, 76.8% for gold, 83.7% for molybdenum in the Pebble East area. Recovery values reflect average results of metallurgical testwork completed to the date of the February 1, 2010 estimate and are subject to revision pending ongoing metallurgical studies. Revenue is calculated for each metal based on grades, recoveries and selected metal prices; accumulated revenues are then divided by the revenue at 1% copper. Recoveries for gold and molybdenum are normalized to the copper recovery as shown below:

CuEq (Pebble West) = Cu % + (Au g/t x 69.6%/85% x 29.00/40.79) + (Mo % x 77.8%/85% x 75.58/40.79)

CuEq (Pebble East) = Cu% + (Au g/t x 76.8%/89.3% x 29.00/40.79)+ (Mo % x 83.7%/89.3% x 5.58/40.79)

2 Individual grades for each metal, as well as estimates for Measured and Indicated resources, are shown in the Mineral Resources section below.

Pebble Project Development Overview

Mine Site Development

As described in the Preliminary Assessment, the Pebble deposit supports an open pit mine utilizing conventional drill, blast and truck-haul methods, with an initial life of 25 years and potential for mine extensions to 78 years and beyond. Phases of mine development beyond 25 years would require separate permitting and development decisions to be made in the future, based on prevailing conditions at the time and the accumulated experience gained from developing and operating the initial phase of the Pebble Project. Near-surface mineral resources in the western portion of the deposit are most efficiently developed through open pit methods, but the potential exists for underground mining (in particular block caving) to emerge as the preferred mining method for subsequent phases of development. Given its size, structure and polymetallic nature, the Pebble deposit presents a great deal of flexibility in near-term and long-term development options.

Of the three development cases, the 25-year IDC Case is the most comprehensively engineered. It seeks to mine near-surface resources for rapid payback, primarily in Measured and Indicated categories but also including a small proportion (16%) of Inferred material. This initial phase of mining processes about two billion tons of material or less than 20% of the total Pebble mineral resource. As such, it is not considered to be ideal for assessing the potential long-term economic value of the Pebble Project.

The level of engineering applied to the 45-year Reference Case is similar to that in the 25-year IDC Case, with the exception of detailed engineering associated with tailings storage after year 25. This extended phase of mining processes some 3.8 billion tons of material (or 32% of the total Pebble mineral resource), primarily in Measured and Indicated categories in the western portion of the deposit. Inferred resources comprise 28% of the total volume mined. Wardrop selected the 45-year Reference Case as the base case for its Preliminary Assessment due to the enhanced level of development of the Pebble mineral resource within a timeframe that makes a significant contribution to the project's NPV. However, the 45-year Reference Case in itself is not an optimized mine plan.

The 78-year Resource Case is based on a continuation of mining methods, costs and assumptions that inform the 25-year IDC Case and the 45-year Reference Case. By developing some 55% of the Pebble mineral resource over eight decades, it is intended to demonstrate the longer-term value of the Pebble Project. The 78-year Resource Case processes some 6.5 billion tons of material, primarily in Measured and Indicated categories from both the western and eastern portions of the Pebble deposit. Inferred resources comprise 33% of the total volume mined.

While the economic valuation of all three development cases is based on open pit mining only, a detailed description of underground block cave mine design, operations, costs and production at a mining rate of 150,000 tons per day is also provided in the Preliminary Assessment.

The Pebble process plant, as described in the Preliminary Assessment, employs conventional crush-grind-float technology and equipment, as well as secondary gold recovery, with a nominal throughput of 200,000 tons per day and the potential to process up to 275,000 tons per day in certain years. Annual throughput averages 219,000 tons per day for the 25-year IDC Case, and 229,000 tons per day for the 45-year Reference Case and 78-year Resource Case.

The grinding circuit comprises two 40 ft x 25 ft @ 29 megawatt semi-autogenous grinding (SAG) mills and four 26 ft x 40 ft @ 16.4 megawatt ball mills. The concentrator produces a copper-gold concentrate containing 26% copper and 18 grams gold per dry tonne, as well as a 52% molybdenum concentrate and gold doré. It is anticipated that the Pebble Partnership would construct a molybdenum autoclave plant offshore to treat the molybdenum concentrate, thereby realizing enhanced value through improved pricing for rhenium and additional copper recovery.

Mine schedules have been developed for the life of mine in each development case, setting out volumes of mineralized and non-mineralized material, densities, tons, dilution, grades of contained metals (copper, gold, molybdenum) and material hardness. A key aspect of these schedules is the annual plant throughput tonnage, which is defined by the grindability of the mineralized material. The rate of production in any given year is derived by that tonnage which utilizes all available energy for which the plant has been designed (909 GWh/a). The production limit of 275,000 tons per day is therefore determined by the SAG mill hydraulic limit. Accordingly, the annual processing rate fluctuates over the mine life as the hardness of the mill feed varies.

Other mine-site facilities and installations include tailings storage, rock storage, a 378 megawatt combined-cycle natural gas-fired turbine plant, as well as shop, office and camp buildings.

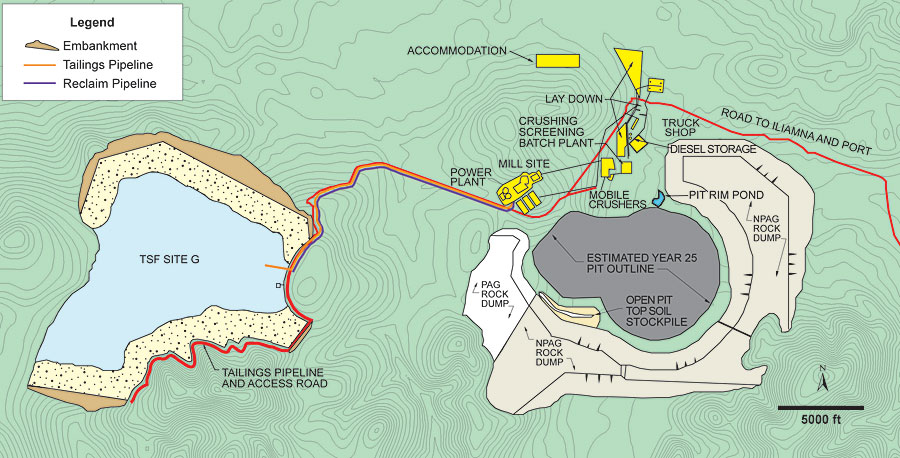

Pebble mine-site layout for the 25-year IDC Case

Copper-gold concentrate produced at Pebble is transported via a slurry pipeline to a new deep-water port on Cook Inlet. There it is de-watered and bulk shipped to offshore smelters. Other products of the process plant are gold doré, which would be flown to market from an existing aviation facility at Iliamna, and molybdenum concentrate, which would be bagged and trucked to the port for shipment.

Process tailings are stored behind purpose-built embankments during mining, and thereafter in the pit. A mine life extension beyond 25 years would require a second tailings storage facility (TSF) to be developed; topographical and land status conditions in the project area present a number of nearby siting opportunities. Engineering has been undertaken to a preliminary level for TSF sites with sufficient capacity to receive mine tailings after 25 years.

The TSF option selected for the 25-year IDC Case is Site G, located approximately three miles west of the open pit. The TSF impoundment would be created by three embankments. The north embankment is constructed initially to a height of approximately 200 feet and raised each year, while the south and east embankments would be built later in the mine life as the impoundment fills. The ultimate height of the north embankment is approximately 685 feet, while ultimate heights for the south and east embankments are approximately 450 feet and 100 feet, respectively.

A site-wide water surplus is forecast at the Pebble Project over the life of the mine. All surplus water would be treated to meet prevailing regulatory standards for water quality and the protection of aquatic life, and released to optimize downstream flow conditions for fish and aquatic habitat.

Infrastructure Development

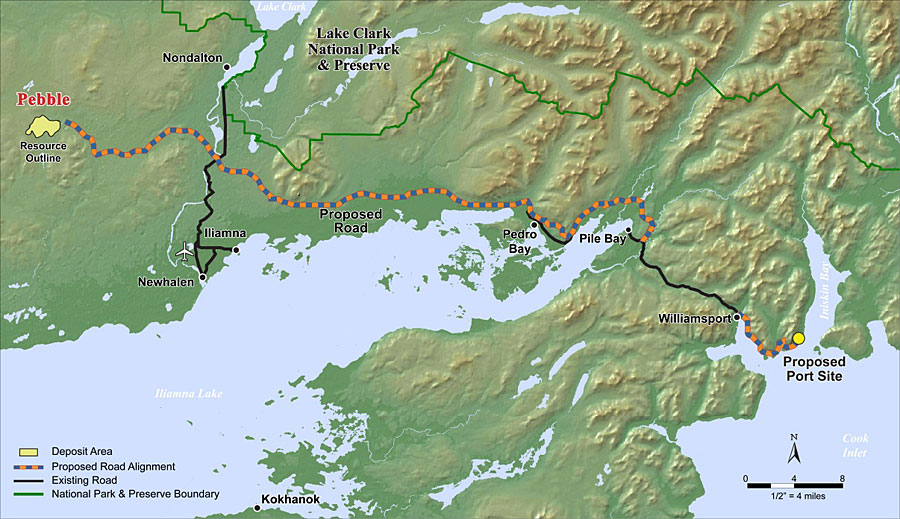

As described in the Preliminary Assessment, an 86-mile transportation corridor would be developed to link the Pebble mine site to a new deep-water port on Cook Inlet, 66 miles to the east, as shown on the local infrastructure map. The transportation corridor includes a two-lane, all-weather permanent access road, whose primary purpose is to transport freight by conventional highway tractors and trailers. The transportation corridor also includes four buried, parallel pipelines, including:

- a copper-gold concentrate slurry pipeline from the mine site to the port;

- a return water pipeline from the port site to the mine;

- a natural gas pipeline from the port site to the mine to fuel a natural gas-fired generating plant at the mine site; and

- a diesel fuel pipeline from the port site to the mine.

Pebble transportation corridor and port site location

A new, permanent deep-water port developed at the entrance to Iniskin Bay on Cook Inlet would serve as a product load-out facility, and facilitate in-bound fuel, equipment and supply shipments. Facilities at the port include a barge dock, deep-sea ship dock, container storage and a handling area for containers. Infrastructure components at the port site include a power generation plant, accommodation and maintenance facilities, offices, fuel storage and transfer facilities. On an annual basis, the port would accommodate shipping of 1.1 million tons of concentrate in Handymax vessels of approximately 50,000 tons, as well as diesel fuel and container barges of equipment and supplies.

Project planning assumes that the nearby Cook Inlet gasfield does not currently have adequate natural gas supplies to meet project needs. Natural gas would be sourced from other regions of Alaska and transported by pipeline from the Kenai Peninsula across Cook Inlet via a sea-bottom line to the port site and along the transportation corridor to the mine site. An alternative is the importation of liquefied natural gas (LNG) directly to the port site. Diesel fuel would be transported via pipeline from the port fuel storage facility to the mine site. In addition to fuelling mobile mining equipment and other rolling stock, emergency electrical generators also operate on diesel fuel.

Project Workforce

Construction of the Pebble Project is projected to take four years, with a peak labour force of 2,080. The operations workforce is projected to average 1,120 over the initial 25-year life of the mine, with longer-term labour requirements to be determined by the mine development alternatives selected. Both construction and operations workforces would be accommodated in project camps at the mine site and the port site, and work on a rotational basis. The Pebble Partnership has stated its intention to maximize local and Alaskan hire at the Pebble Project, and is developing a workforce development plan to accomplish this goal.

Production Profiles

The 45-year Reference Case processes 3.8 billion tons of mineralized material, with a strip ratio of 2.1:1 and average grades of 0.46% copper, 0.011 oz gold per ton and 214 ppm molybdenum. Metallurgical recoveries average 87.9% for copper, 71.3% for gold and 87.9% for molybdenum. Over the life of mine, the 45-year Reference Case produces 30.5 billion lb of copper, 30.3 million oz of gold and 1.4 billion lb of molybdenum, as well as 140 million oz of silver, 1.2 million kg of rhenium and 907,000 oz of palladium.

Production results for all three development cases are presented in the table below:

| Item | Unit | IDC Case | Reference Case | Resource Case |

|---|---|---|---|---|

| Mine Life | years | 25 | 45 | 78 |

| Mining Method | Open Pit | Open Pit | Open Pit | |

| Strip Ratio | waste : ore | 1.5 | 2.1 | 2.6 |

| Processing Rate | M ton / yr | 80 | 84 | 84 |

| Total Processed | M ton | 1,990 | 3,767 | 6,528 |

| % of M+I+I Resource | % | 17 | 32 | 55 |

| Copper Eq. Grade | % | 0.72 | 0.83 | 0.84 |

| Copper Grade | % | 0.38 | 0.46 | 0.46 |

| Gold Grade | oz / ton | 0.012 | 0.011 | 0.011 |

| Molybdenum Grade | ppm | 182 | 214 | 243 |

| Copper Recovery | % | 86.6 | 87.9 | 88.4 |

| Gold Recovery | % | 71.5 | 71.3 | 71.2 |

| Molybdenum Recovery | % | 84.8 | 87.9 | 89.4 |

| Copper Eq. Recovered | M lb | 24,483 | 54,129 | 96,357 |

| Copper Recovered | M lb | 12,944 | 30,494 | 53,437 |

| Gold Recovered | 000 oz | 16,391 | 30,307 | 50,133 |

| Molybdenum Recovered | M lb | 616 | 1,420 | 2,835 |

| Peak Annual Copper Recovered | M lb | 822 | 1,157 | 1,096 |

| Peak Annual Gold Recovered | 000 oz | 1,038 | 1,127 | 1,088 |

| Peak Annual Molybdenum Recovered | M lb | 43 | 56 | 62 |

| Avg Annual Copper Recovered | M lb | 518 | 678 | 685 |

| Avg Annual Gold Recovered | 000 oz | 656 | 673 | 643 |

| Avg Annual Molybdenum Recovered | M lb | 25 | 32 | 36 |

| 26% Cu-Au Concentrate Produced | 000’s dmt | 22,582 | 53,200 | 93,225 |

| 52% Mo Concentrate Produced | 000’s dmt | 537 | 1,239 | 2,473 |

Financial Valuation

Pebble Project

Economic valuations for all three development cases presented in the Preliminary Assessment are expressed in US dollars in real terms. The valuation date for NPV, IRR and other financial results is at the commencement of project construction.

Long-term and current prevailing metal prices applied to the financial model for each of the development cases are outlined in the table below:

| Metal Type | Unit | Long Term Metal Prices | Current Prevailing Metal Prices |

|---|---|---|---|

| Copper | $/lb | 2.50 | 4.00 |

| Gold | $/oz | 1,050 | 1,350 |

| Molybdenum | $/lb | 13.50 | 15.00 |

| Silver | $/oz | 15.00 | 28.00 |

| Rhenium | $/kg | 3,000 | 3,000 |

| Palladium | $/oz | 490 | 490 |

Net Smelter Return (NSR) statistics at long-term metal prices for all three development cases are provided in the table below:

| Description | Unit | IDC Case 25 years |

Reference Case 45 years |

Resource Case 78 years |

|---|---|---|---|---|

| NSR LOM | $ M | 54,637 | 120,197 | 213,970 |

| NSR Annual Average | $ M | 2,185 | 2,671 | 2,743 |

| Copper | % | 52 | 55 | 55 |

| Gold | % | 29 | 24 | 22 |

| Molybdenum | % | 15 | 16 | 18 |

| Other | % | 4 | 5 | 5 |

| NSR per ton milled | $ / ton | 27.45 | 31.91 | 32.78 |

Annual cash flows are calculated and subsequently discounted at a rate of 7%. Market convention generally uses a discount rate of 8% for copper and other base metal projects and 5% for gold and other precious metal projects. Given the large contribution of gold to total revenues at the Pebble Project, a 7% blended discount rate has been selected. Financial results for all three development cases are summarized below:

| Item | Unit | IDC Case | Reference Case | Resource Case |

|---|---|---|---|---|

| Mine Life | years | 25 | 45 | 78 |

| Initial Capital | $ M | 4,695 | 4,695 | 4,695 |

| LOM Sustaining Capital | $ M | 3,204 | 6,140 | 11,727 |

| LOM NSR | $ M | 54,637 | 120,197 | 213,970 |

| NSR Per Ton | $ / ton | 27.45 | 31.91 | 32.78 |

| LOM Operating Cost | $ M | 22,208 | 43,489 | 96,063 |

| Operating Cost Per Ton | $ / ton | 11.16 | 11.55 | 14.72 |

| C1 Copper Cost | $ / lb | -0.10 | -0.11 | 0.21 |

| LOM Pre-Tax Net Cash Flow | $ M | 20,123 | 55,278 | 87,329 |

| Long-term Metal Prices | ||||

| Pre-Tax NPV at 7% | $ M | 3,837 | 6,129 | 6,812 |

| Pre-Tax IRR | % | 13.4% | 14.2% | 14.5% |

| Pre-Tax Payback | years | 6.5 | 6.2 | 6.1 |

| Current Prevailing Metal Prices | ||||

| Pre-Tax NPV at 7% | $ M | 11,410 | 15,709 | 16,864 |

| Pre-Tax IRR | % | 22.6% | 23.2% | 23.3% |

| Pre-Tax Payback | years | 3.2 | 3.2 | 3.2 |

Pre-tax results are before income taxes but after net profits interest (NPI) royalty and local production taxes.

C1 Copper Cost is the cash cost per payable pound of copper (including operating costs and realization charges) after by-product credits

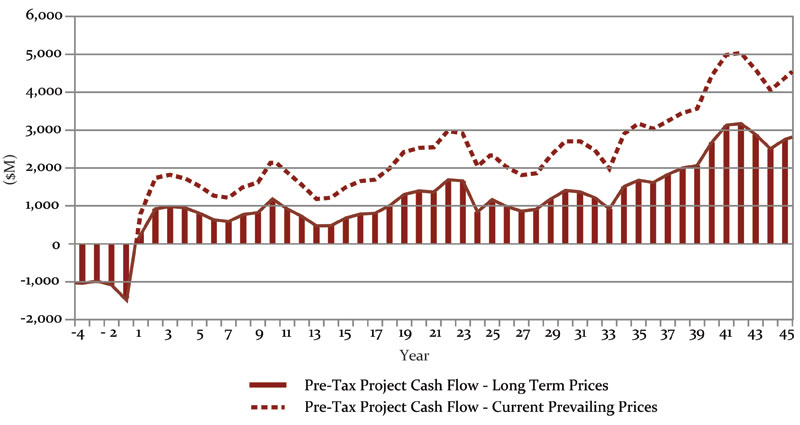

Annual pre-tax cash flows for the 45-year Reference Case are illustrated in the figure below.

Northern Dynasty's 50% Interest

Under the terms of the Pebble Limited Partnership Agreement, Anglo American is required to elect to commit $1.425 to $1.5 billion in staged investments in order to retain its 50% interest in the Pebble Project. If a feasibility study for the project is completed after 2011, Anglo American's overall funding requirement increases from $1.425 billion to $1.5 billion. A significant proportion of Anglo American's financial contribution is expected to be applied to initial capital costs to construct the mine, thereby reducing Northern Dynasty's capital requirements.

In order to calculate an NPV and IRR estimate for Northern Dynasty's 50% interest in the Pebble Project under this scenario, it is necessary to adjust Northern Dynasty's share of initial capital costs. For the purpose of this calculation, it is assumed that $1 billion of Anglo American's funding requirement would be applied to the Pebble Project's capital cost for construction. To the end of 2010, Anglo American has invested some $325 million to advance the Pebble Project.

Inasmuch as Northern Dynasty is in a position to calculate taxes payable for its portion of profits associated with development of the Pebble Project, financial results for Northern Dynasty's 50% interest in the project have been presented on a pre-tax and post-tax basis, and at long-term and current prevailing metal prices, in the table below:

| Item | Unit | IDC Case | Reference Case | Resource Case |

|---|---|---|---|---|

| Long-term Metal Prices | ||||

| Pre-Tax NPV at 7% | $ M | 2,403 | 3,550 | 3,891 |

| Pre-Tax IRR | % | 17.3 | 18.0 | 18.4 |

| Pre-Tax Payback | years | 4.9 | 4.7 | 4.6 |

| Current Prevailing Metal Prices | ||||

| Pre-Tax NPV at 7% | $ M | 6,190 | 8,339 | 8,917 |

| Pre-Tax IRR | % | 29.5 | 30.2 | 30.4 |

| Pre-Tax Payback | years | 2.7 | 2.6 | 2.6 |

| Long-term Metal Prices | ||||

| Post-Tax NPV at 7% | $ M | 1,559 | 2,358 | 2,650 |

| Post-Tax IRR | % | 14.6 | 15.4 | 15.8 |

| Post-Tax Payback | years | 5.6 | 5.3 | 5.3 |

| Current Prevailing Metal Prices | ||||

| Post-Tax NPV at 7% | $ M | 4,141 | 5,561 | 6,002 |

| Post-Tax IRR | % | 24.5 | 25.1 | 25.4 |

| Post-Tax Payback | years | 3.1 | 3.1 | 3.0 |

Pre-tax results are before income taxes but after NPI royalty and local production taxes.

The impact of various discount rates on Northern Dynasty's 50% share of the Pebble Project's pre-tax NPV7, and its sensitivity to a range of copper and gold prices (both individually and combined with other metal prices held constant) is presented in the table below. Life of Mine cash flow for Northern Dynasty's 50% is $7,535 million for the 25-year IDC Case, $19,818 million for the 45-year Reference Case and $31,583 million for the 78-year Resource Case.

| Item | Unit | IDC Case | Reference Case | Resource Case |

|---|---|---|---|---|

| Discount Rate | ||||

| NPV at 5% | $M | 2,491 | 4,164 | 4,877 |

| NPV at 7% | $M | 1,559 | 2,358 | 2,650 |

| NPV at 8% | $M | 1,213 | 1,774 | 1,975 |

| NPV at 10% | $M | 689 | 976 | 1,087 |

| Copper Price (Gold $1050/oz, Mo $13.50/lb) | ||||

| 2.50 | $M | 1,559 | 2,358 | 2,650 |

| 2.75 | $M | 1,893 | 2,776 | 3,089 |

| 3.00 | $M | 2,226 | 3,192 | 3,525 |

| 3.25 | $M | 2,557 | 3,605 | 3,955 |

| 3.50 | $M | 2,874 | 4,006 | 4,375 |

| 3.75 | $M | 3,188 | 4,404 | 4,792 |

| 4.00 | $M | 3,499 | 4,796 | 5,201 |

| 4.25 | $M | 3,802 | 5,181 | 5,605 |

| Gold Price (Copper $2.50/lb, Mo $13.50/lb) | ||||

| 1050 | $M | 1,559 | 2,358 | 2,650 |

| 1100 | $M | 1,646 | 2,459 | 2,755 |

| 1150 | $M | 1,733 | 2,560 | 2,860 |

| 1200 | $M | 1,820 | 2,660 | 2,964 |

| 1250 | $M | 1,906 | 2,760 | 3,068 |

| 1300 | $M | 1,993 | 2,861 | 3,172 |

| 1350 | $M | 2,079 | 2,961 | 3,276 |

| 1400 | $M | 2,166 | 3,061 | 3,380 |

| Combined Copper and Gold Price (Mo $13.50/lb) | ||||

| 2.50 / 1050 | $M | 1,559 | 2,358 | 2,650 |

| 2.75 / 1100 | $M | 1,980 | 2,876 | 3,193 |

| 3.00 / 1150 | $M | 2,399 | 3,391 | 3,732 |

| 3.25 / 1200 | $M | 2,804 | 3,895 | 4,255 |

| 3.50 / 1250 | $M | 3,200 | 4,389 | 4,771 |

| 3.75 / 1300 | $M | 3,590 | 4,873 | 5,276 |

| 4.00 / 1350 | $M | 3,971 | 5,350 | 5,776 |

| 4.25 / 1400 | $M | 4,351 | 5,827 | 6,276 |

Capital and Operating Costs

Initial and Sustaining Capital

All three development cases presented in the Preliminary Assessment have the same initial capital requirement of $4.7 billion. This includes:

- direct field costs for executing the project;

- indirect costs associated with the design, construction and commissioning of new facilities;

- owner's support costs for corporate, environmental, permitting and staffing; and

- capital costs to completion of construction and commissioning at the end of Year -1.

The capital cost estimate has been developed over a series of project stages and is largely based on first principles estimates. Quantities have been derived for project components for which productivity and labour rates have been estimated for specific trades. As a result, the capital cost estimate approaches a pre-feasibility level of accuracy.

It has been anticipated in the financial valuation that the Pebble Partnership would enter into strategic partnerships as needed to develop, finance and operate a number of infrastructure assets -- including the transportation corridor (port and road) and the power plant. Each financial case also considers that the Pebble Partnership would construct a molybdenum autoclave plant offshore to treat the molybdenum concentrate, and thereby realize enhanced value through improved pricing for rhenium and additional copper recovery. Other costs include owner's costs and an overall capital cost contingency of 17.7%.

The initial capital cost for all three development cases is shown in the table below:

| Area | Cost ($M) |

|---|---|

| Mining | 430.8 |

| Processing | 1,389.3 |

| Other Infrastructure | 422.0 |

| Tailings | 294.0 |

| Pipelines | 97.5 |

| Access Road * | 162.0 |

| Port Infrastructure * | 154.5 |

| Power Generation * | 534.1 |

| Indirect Costs | 1,406.8 |

| Contingency | 865.7 |

| Molybdenum Autoclave | 374.2 |

| Less: Escalation/ De-Escalation | (121.1) |

| Less: Outsourced Infrastructure * | (1,315.0) |

| Total | 4,694.8 |

*Outsourced infrastructure, including associated indirects and contingencies

Sustaining capital requirements (in $M) for all three development cases are shown in the table below:

| Area | IDC Case | Reference Case | Resource Case |

|---|---|---|---|

| Open Pit | 2,047 | 3,286 | 7,225 |

| Processing | 146 | 230 | 517 |

| Infrastructure | 12 | 165 | 165 |

| Waste Management | 846 | 2,211 | 3,364 |

| Other | 70 | 104 | 180 |

| Molybdenum Autoclave | 83 | 144 | 276 |

| Total | 3,204 | 6,140 | 11,727 |

Operating Costs

Life of mine unit operating costs for the 45-year Reference Case are estimated to be $11.55 per ton milled. This includes all costs associated with open pit mining of mineralized and non-mineralized material, processing of mill feed to a final concentrate and all services required to support the operation. This estimate has been prepared as an annual cost for each year of the project from plant start-up to mine closure. Operating costs are based on estimated process plant throughput rates, which range depending on the grindability of the material fed to the process plant.

Life of mine unit operating costs for all three development cases are presented in the table below:

| Description | Unit | IDC Case | Reference Case | Resource Case |

|---|---|---|---|---|

| Total Operating Costs | $M | 22,208 | 43,489 | 96,063 |

| Open Pit | $ / ton | 3.83 | 4.30 | 7.19 |

| Process | $ / ton | 4.50 | 4.60 | 4.93 |

| Transportation | $ / ton | 0.97 | 0.91 | 0.91 |

| Environmental | $ / ton | 0.30 | 0.29 | 0.31 |

| G&A | $ / ton | 1.56 | 1.45 | 1.38 |

| Total Operating Costs per ton milled | $ / ton | 11.16 | 11.55 | 14.72 |

Costs of ocean freight for the transportation of final concentrate to off-shore smelters, as well as all smelter and other offsite charges, are summarized in the table below:

| Description | Unit | IDC Case | Reference Case | Resource Case |

|---|---|---|---|---|

| Offsite Charges | ||||

| Total Offsite Charges | $ M | 4,752 | 11,089 | 19,938 |

| Offsite Charges per ton milled | $ / ton | 2.39 | 2.94 | 3.05 |

| Cash Cost Analysis | ||||

| Offsite Charges | $/lb | 0.38 | 0.38 | 0.39 |

| Operating Costs | $/lb | 1.79 | 1.48 | 1.87 |

| Copper Cash Cost | $/lb | 2.17 | 1.86 | 2.26 |

| By-Product Credits | $/lb | -2.27 | -1.97 | -2.05 |

| C1 Copper Cost | $/lb | -0.10 | -0.11 | 0.21 |

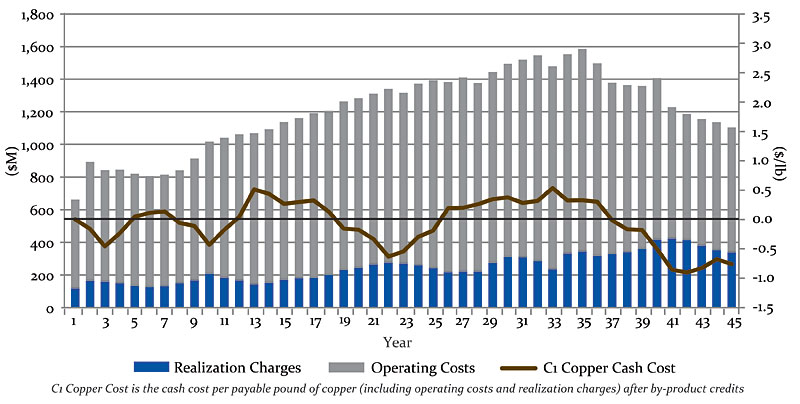

Annual costs for the 45-year Reference Case are summarized in the figure below.

Mineral Resources

Mineralization within the Pebble deposit is dominated by hypogene pyrite, chalcopyrite and molybdenite. Bornite is also an important component in some parts of the Pebble East zone. The Pebble West zone has a thin, volumetrically subordinate zone of supergene mineralization and a very minor zone of oxide mineralization. The Pebble East zone contains only hypogene mineralization.

Copper-gold-molybdenum mineralization, as currently known, extends over an east-west elongated area of 2.8 by 1.9 miles and to a depth of 2,000 feet in the Pebble West zone, and to at least 5,000 feet in the Pebble East zone. Mineralization in the Pebble East zone remains open to the east, north and south. A much larger zone of strong alteration and low-grade mineralization extends north, south and west of the known Pebble deposit.

The current Pebble mineral resource estimate (see Northern Dynasty news release dated February 1, 2010) represents the culmination of seven years of geological and geostatistical analysis and is based on drill data to September 2009.

The Pebble deposit mineral resources are reported within a defined volume at various cut-off grades in the table below:

| Cut-off (% CuEQ) | CuEQ (%) | Mt | Cu (%) | Au (g/t) | Mo (ppm) | Cu (Blb) | Au (Moz) | Mo (Blb) | CuEq (Blb) |

|---|---|---|---|---|---|---|---|---|---|

| Measured | |||||||||

| 0.30 | 0.65 | 527 | 0.33 | 0.35 | 178 | 3.8 | 5.9 | 0.21 | 7.6 |

| 0.40 | 0.66 | 508 | 0.34 | 0.36 | 180 | 3.8 | 5.9 | 0.20 | 7.4 |

| 0.60 | 0.77 | 277 | 0.40 | 0.42 | 203 | 2.4 | 3.7 | 0.12 | 4.7 |

| 1.00 | 1.16 | 27 | 0.62 | 0.62 | 301 | 0.4 | 0.5 | 0.02 | 0.7 |

| Indicated | |||||||||

| 0.30 | 0.80 | 5,414 | 0.43 | 0.35 | 257 | 51.3 | 60.9 | 3.07 | 95.5 |

| 0.40 | 0.85 | 4,891 | 0.46 | 0.36 | 268 | 49.6 | 56.6 | 2.89 | 91.7 |

| 0.60 | 1.00 | 3,391 | 0.56 | 0.41 | 301 | 41.9 | 44.7 | 2.25 | 74.8 |

| 1.00 | 1.30 | 1,422 | 0.77 | 0.51 | 342 | 24.1 | 23.3 | 1.07 | 40.7 |

| Measured + Indicated | |||||||||

| 0.30 | 0.78 | 5,942 | 0.42 | 0.35 | 250 | 55.0 | 66.9 | 3.28 | 102.2 |

| 0.40 | 0.83 | 5,399 | 0.45 | 0.36 | 260 | 53.6 | 62.5 | 3.09 | 98.8 |

| 0.60 | 0.98 | 3,668 | 0.55 | 0.41 | 293 | 44.5 | 48.3 | 2.37 | 79.2 |

| 1.00 | 1.29 | 1,449 | 0.76 | 0.52 | 341 | 24.3 | 24.2 | 1.09 | 41.2 |

| Inferred | |||||||||

| 0.30 | 0.53 | 4,835 | 0.24 | 0.26 | 215 | 25.6 | 40.4 | 2.29 | 56.5 |

| 0.40 | 0.66 | 2,845 | 0.32 | 0.30 | 259 | 20.1 | 27.4 | 1.62 | 41.4 |

| 0.60 | 0.89 | 1,322 | 0.48 | 0.37 | 289 | 14.0 | 15.7 | 0.84 | 25.9 |

| 1.00 | 1.20 | 353 | 0.69 | 0.45 | 379 | 5.4 | 5.1 | 0.29 | 9.3 |

Details of CuEQ calculations are provided in the note under Preliminary Assessment Key Findings above.

Opportunities

Wardrop has identified a number of opportunities that could add substantial additional value to the Pebble Project. It is Northern Dynasty's expectation that these opportunities will be investigated in subsequent stages of project planning, and include:

- Numerous compelling exploration targets exist within the 186 square mile Pebble property claim boundary. Immediately adjacent to the Pebble deposit and east of the resource-bounding ZG1 fault is the high-grade intersection in drill hole 6348 (949 feet at 1.92% CuEq3 ). The area to the east of this intersection remains completely open.

Outside the Pebble deposit, two seasons of exploration drilling have identified numerous zones of copper, gold, molybdenum and silver mineralization. These include the 'No. 1' gold showing, the '25 zone', the '52 Porphyry zone', the '308 Porphyry zone', the '37 Skarn zone' and the '65 zone'. In addition, several zones of strong alteration and elevated levels of Cu-Mo or Au-Zn-Ag indicate that new, entirely separate porphyry-style mineralizing centres occur. These deposits and high-priority targets present near-term opportunities to expand and enhance known mineral resources on the Pebble property.

- Portions of the Pebble deposit have superior silver grades that have not yet been optimized.

- The volume and geo-metallurgy of the Pebble deposit presents a number of opportunities to optimize the project over the mine life, or to amend the mine plan in response to prevailing market conditions.

- The open pit shells used in the Preliminary Assessment were generated using parameters developed in early 2009. A number of these parameters (e.g. metal prices of $1.80/lb copper, $800/oz gold and $10/lb molybdenum) have seen significant improvement, which should be incorporated into the pit optimization during the next study phase.

- Pit walls could be steepened from the current 39° slope to 41°, resulting in a net waste rock reduction of approximately 30 million tons in the 25-year IDC Case, and more in the 45-year Reference Case and 78-year Resource Case.

- An extended period of low stripping after year 45 indicates the sequencing of the 45-year open pit could be optimized by reducing the strip ratio leading into the mining of the later ore. Further, the value demonstrated by the 78-year Resource Case demonstrates that running the pit optimization over the life of the project may further increase project returns.

- The use of autonomous trucks has been shown to add significant value to the Pebble Project. Additional automation opportunities, such as blasthole drilling and plant automation, will likely have analogous benefits.

- Underground mine development has not been considered as a primary case in the Preliminary Assessment. Further assessment of this option is fully warranted, including through development of an early access shaft during the initial 25 years of mining, to evaluate methodologies for determining relative economics of an underground mine and confirming its performance through feasibility-level studies.

- The 40 foot SAG mills selected for the Pebble Project are the largest currently in operation; however, a 42 foot diameter mill has recently been ordered for another project. Application of 42 foot SAG mills would enhance both throughput and NPV at the Pebble Project.

- Some porphyry projects report higher gold recoveries than are projected for Pebble. Gold recoveries can be increased by reducing the copper grade within the copper-gold concentrate. Inasmuch as a 5% increase in gold recovery would enhance the NPV of the 45-year Reference Case by some $300 million, trade-off analysis of this opportunity should be conducted during the next phase of study.

- In the current grinding circuit layout, crushed pebbles are returned to the SAG mill (SABC-A circuit). An analysis has determined that returning crushed pebbles to the ball mills (SABC-B circuit) could increase mill throughput by 5 - 10%. A 5% improvement in throughput would increase the NPV of the 45-year Reference Case by some $600 million.

- Due to its size, the Pebble deposit can accommodate a significantly higher mill throughput than is currently proposed. Previous analyses have shown the beneficial financial impact of higher throughput rates, and warrant further study.

- Wardrop has reviewed the methodology used to develop the capital cost estimate and believes certain costs may have been overestimated. Based on a preliminary, high-level estimate of the likely range of capital cost outcomes, savings of some $362 million were identified. For Northern Dynasty's 50% share of the project, this capital cost reduction would result in an increase in post-tax IRR to 16.7%, and an increase in its post-tax NPV7 to $2,486 million. Wardrop anticipates that further cost savings are possible through engineering optimization.

- Alternative port construction techniques may add value to the Pebble Project, such as building the facility as caissons to be towed to site and ballasted to the seafloor.

- A range of opportunities exist to outsource additional elements of the Pebble Project to enhance project economics and provide opportunities for local businesses. These include: air transport; concentrate and water return pipelines; mine and port site accommodation facilities; freight transport between the port site and the mine site; local transportation, at the mine site and between the mine site and local villages; turn-key fuel supply; and mine equipment maintenance, among others.

3 1.24% Cu, 0.74 g/t Au and 0.024% Mo and calculated using $1.00/lb for Cu, $400/oz for Au and $6.00/lb for Mo.

Going Forward

The Pebble Project would be a large industrial facility located within a vast region of Alaska notable for its undeveloped wilderness, isolated and sparsely populated communities, Alaska Native culture and traditional ways of life, significant salmon fisheries, and other fish and wildlife populations. Since 2004, Northern Dynasty and subsequently the Pebble Partnership have undertaken a comprehensive stakeholder outreach program to document the priorities and concerns of local communities and area residents, and facilitate their participation in the process by which the Pebble Project will be designed, permitted, built and operated.

Concurrently, extensive baseline studies have been undertaken to characterize the physical, chemical, biological and social environment of the project area. These studies have resulted in a superior database, which -- in characterizing the climate, surface and groundwater hydrology, wetlands, terrestrial wildlife habitat, fish and aquatic habitat, and marine habitat -- has guided all aspects of project planning. The findings of these exhaustive studies will be compiled in an Environmental Baseline Document planned to be publicly released in early 2011.

The Pebble Partnership continues to advance engineering and project design initiatives for the Pebble Project. This effort will be informed by input received from project stakeholders through public consultation forums undertaken in Alaska prior to the completion of a Prefeasibility Study and the submission of permit applications. At this time, it is expected that the Pebble Partnership will complete a Prefeasibility Study for the Pebble Project in 2012, prior to initiating permitting under NEPA.

Permitting will be initiated when the Pebble Partnership submits its Project Description and Environmental Baseline Document. These documents will provide the basis for an Environmental Impact Statement (EIS) to be prepared. The EIS will be prepared by a third-party contractor under the direction of a lead federal agency. The Pebble EIS will be the focal point for project permitting. It will determine whether sufficient evaluation of the project's environmental effects and development alternatives has been undertaken, and provide the basis for federal, state and local government agencies to make individual permitting decisions.

Management Discussion

The Pebble Project is a superior, long-life mineral development opportunity of strategic global importance. As presented in the Preliminary Assessment, project economics are robust and support a mine development that is both technically feasible and permittable under existing regulatory standards in Alaska. Further, the Pebble Project is being designed to achieve international best practice standards of design and performance, such that key environmental and cultural values are protected and meaningful development benefits accrue to local communities, the State of Alaska and the United States of America.

The Pebble deposit is located on state land in southwest Alaska that has been subject to two comprehensive land-use planning exercises, and subsequently designated for mineral exploration and development. As a jurisdiction, Alaska has a long history of responsible natural resource development, and environmental standards and permitting requirements that are stable, objective, rigorous and science-based.

Since 2004, comprehensive environmental and socioeconomic baseline studies have been undertaken in the Pebble Project area, including along the transportation corridor to Cook Inlet, the marine environment in the area of the port site and throughout the broader Bristol Bay region. These studies have cost more than $150 million to date, and resulted in an environmental and socioeconomic database whose comprehensiveness and depth is unprecedented in Alaska. The aggregated findings and analyses of these studies, along with the Pebble Partnership's ongoing, long-term engagement with project stakeholders and federal and state regulators, are significant corporate assets as it prepares the Pebble Project for permitting.

The Pebble Project has the potential to generate significant direct and indirect employment, business and economic activity, and government revenues in the Bristol Bay region, the State of Alaska and the United States. The Pebble Partnership has a stated intention to maximize project benefits for the residents and communities of southwest Alaska, and is developing long-term workforce and business development strategies to realize this goal. Transportation and energy infrastructure development associated with the Pebble Project also has the potential to deliver significant benefits for local communities, by lowering the cost of living and supporting economic growth and diversification. Pebble also has the potential to contribute to the health and value of local fisheries by enhancing natural habitat productivity, and providing power and transportation benefits to enhance product quality. Meaningful benefits associated with power generation and transmission, in particular, could be extended to communities throughout the Bristol Bay region.

Qualified Persons

Wardrop Engineering Inc. was commissioned exclusively by Northern Dynasty to prepare a Preliminary Assessment Technical Report of the Pebble Project, based on its review of recent engineering and technical studies undertaken by the Pebble Partnership and Northern Dynasty, as provided and verified by Northern Dynasty. The Pebble Project Preliminary Assessment conforms to the standards set out in National Instrument 43 101 (Standards and Disclosure for Mineral Projects) and is in compliance with Form 43-101F1.

A summary of the Qualified Persons responsible for various sections of the Preliminary Assessment are identified in the table below. All are independent of Northern Dynasty. The contents of this news release has been reviewed and approved by all listed Qualified Persons.

| Report Section | Qualified Person | |

|---|---|---|

| Company | Qualified Person | |

| 1.0 – Executive Summary | Wardrop | Hassan Ghaffari, P.Eng. |

| 2.0 – Introduction | Wardrop | Hassan Ghaffari, P.Eng. |

| 3.0 – Reliance on Other Experts | Wardrop | Hassan Ghaffari, P.Eng. |

| 4.0 – Property Description and Location | Wardrop | Robert Morrison, P.Geo. |

| 5.0 – Accessibility, Climate, Local Resources, Infrastructure, and Physiography |

Wardrop | Robert Morrison, P.Geo. |

| 6.0 – History | Wardrop | Robert Morrison, P.Geo. |

| 7.0 – Geological Setting | Wardrop | Robert Morrison, P.Geo. |

| 8.0 – Deposit Types | Wardrop | Robert Morrison, P.Geo. |

| 9.0 – Mineralization | Wardrop | Robert Morrison, P.Geo. |

| 10.0 – Exploration | Wardrop | Robert Morrison, P.Geo. |

| 11.0 – Drilling | Wardrop | Robert Morrison, P.Geo. |

| 12.0 – Sampling Method and Approach | Wardrop | Robert Morrison, P.Geo. |

| 13.0 – Sample Preparation, Analyses and Security | Wardrop | Robert Morrison, P.Geo. |

| 14.0 – Data Verification | Wardrop | Robert Morrison, P.Geo. |

| 15.0 – Adjacent Properties | Wardrop | Robert Morrison, P.Geo. |

| 16.0 – Mineral Processing | Wardrop | Andre de Ruijter, P.Eng/ Hassan Ghaffari, P.Eng. |

| 17.0 – Mineral Resource and Mineral Reserve Estimates | Wardrop | Robert Morrison, P.Geo. |

| 18.0 – Other Relevant Data and Information | ||

| 18.1 – Mining | Wardrop | Tysen Hantelmann, P.Eng. |

| 18.2 – Infrastructure | Wardrop | Hassan Ghaffari, P.Eng. |

| 18-3 – Tailings, Waste Rock, and Water Management | Wardrop | Aleksandar Zivkovic, P.Eng. |

| 18.4 – Sustainability | Wardrop | Doug Ramsey, P.R. Bio |

| 18.5 – Capital Cost Estimate | Wardrop | Hassan Ghaffair, P.Eng., Tysen Hantelmann, P.Eng., Aleksandar Zivkovic, P.Eng. |

| 18.6 – Operating Cost Estimate | Wardrop | Andre de Ruijter, P.Eng., Tysen Hantelmann, P.Eng. |

| 18.7 – Project Execution Plan | Wardrop | Hassan Ghaffari, P.Eng. |

| 18.8 – Financial Analysis | Wardrop | Scott Cowie, MAusIMM |

| 19.0 – Interpretation and Conclusions | Wardrop | All; sign off by discipline |

| 20.0 – Opportunities and Recommendations | Wardrop | All; sign off by discipline |

About Northern Dynasty

Northern Dynasty Minerals Ltd. is a mineral exploration and development company based in Vancouver, Canada, with direct and indirect interests in 592 square miles of mineral claims in southwest Alaska. Northern Dynasty's principal asset is a 50% interest in the Pebble Limited Partnership, owner of the Pebble Copper-Gold-Molybdenum Project. The Pebble Project is an advanced-stage initiative to develop one of the most important mineral resources in the world.

About the Pebble Project

The Pebble Project is an initiative of the Pebble Partnership to responsibly develop a globally significant copper, gold and molybdenum deposit in southwest Alaska into a modern, long-life mine. The project is located 200 miles southwest of Anchorage on state land designated for mineral exploration and development. It is situated approximately 1,000 feet above sea-level, 65 miles from tidewater on Cook Inlet and presents favourable conditions for successful mine site and infrastructure development.

The Pebble Project consists of the Pebble deposit, surrounding mineral claims and a stream of financing provided by Northern Dynasty's project partner Anglo American US (Pebble) LLC. The Pebble Partnership was established in July 2007 as a 50:50 partnership between a wholly-owned affiliate of Northern Dynasty and a wholly-owned subsidiary of Anglo American plc. Both Northern Dynasty and Anglo American have equal and identical rights of management, operatorship and control in the Pebble Partnership.

Under the terms of the Pebble Limited Partnership Agreement, Anglo American is required to elect to commit $1.425 to $1.5 billion in staged investments in order to retain its 50% interest in the Pebble Project. If a feasibility study for the Pebble Project is completed after 2011, Anglo American's overall funding requirement increases from $1.425 billion to $1.5 billion. Funds provided by Anglo American are currently being invested in comprehensive exploration, engineering, environmental and socioeconomic programs toward the future development of the Pebble Project.

For further details on Northern Dynasty please visit the Company's website at www.northerndynasty.com or contact Investor services at (604) 684-6365 or within North America at 1-800-667-2114. Review Canadian public filings at www.sedar.com and US public filings at www.sec.gov.

Ronald W. Thiessen

President & CEO

Sole Responsibility

No regulatory authority accepts responsibility for the adequacy or accuracy of this release.

Northern Dynasty is solely and entirely responsible for the contents of this news release. No other party, including any parties which have an interest in the project, are in any way responsible for the contents hereof.

Forward Looking Information and other Cautionary Factors

All information contained in this press release relating to the contents of the Preliminary Assessment, including but not limited to statements of the Pebble Project's potential and information under the headings "Preliminary Assessment Key Findings," "Production Profiles," "Financial Valuation" and "Capital and Operating Costs" are "forward looking statements" within the definition of the United States Private Securities Litigation Reform Act of 1995. The information relating to the possible construction of a port, road, power generating facilities and power transmission facilities also constitutes such "forward looking statements." The Preliminary Assessment was prepared to broadly quantify the Pebble project's capital and operating cost parameters and to provide guidance on the type and scale of future project engineering and development work that will be needed to ultimately define the project's likelihood of feasibility and optimal production rate. It was not prepared to be used as a valuation of the Pebble project nor should it be considered to be a pre-feasibility study. Although based on a comprehensive technical review of recent engineering and technical studies undertaken by the Pebble Partnership and Northern Dynasty, the studies of capital and operating costs are incomplete and have not been optimized, so the ultimate costs may vary widely from the amounts set out in the Preliminary Assessment. This could materially and adversely impact the projected economics of the Pebble project. The Preliminary Assessment, in part, uses inferred mineral resources which are considered too speculative geologically to be categorized as mineral reserves and to have economic considerations applied to them. There can be no assurance that the operating and financial projections contained in the Preliminary Assessment will be realized.

The following are the principal risk factors and uncertainties which, in management's opinion, are likely to most directly affect the conclusions of the Preliminary Assessment and the ultimate feasibility of the Pebble project. A portion of the mineralized material at the Pebble Project is currently classified as an inferred resource and it is not a reserve. The mineralized material in the Preliminary Assessment is based on the measured, indicated and inferred resources estimated by Hunter Dickinson Inc. and audited by Wardrop. Additional process tests and other engineering and geologic work will be required to determine if the mineralized material is an economically exploitable reserve. There can be no assurance that this mineralized material can become a reserve or that the amount may be converted to a reserve or the grade thereof. Final feasibility work has not been done to confirm the pit design, mining methods, and processing methods assumed in the Preliminary Assessment. Final feasibility could determine that the assumed pit design, mining methods, and processing methods are not correct. Construction and operation of the mine and processing facilities depends on securing environmental and other permits on a timely basis. No permits have been applied for and there can be no assurance that required permits can be secured or secured on a timely basis. Data is incomplete and cost estimates have been developed in part based on the expertise of the individuals participating in the preparation of the Preliminary Assessment and on costs at projects believed to be comparable, and not based on firm price quotes. Costs, including design, procurement, construction, and on-going operating costs and metal recoveries could be materially different from those contained in the Preliminary Assessment. There can be no assurance that mining can be conducted at the rates and grades assumed in the Preliminary Assessment. The project requires the development of port facilities, roads and electrical generating and transmission facilities. Although Northern Dynasty believes that the State of Alaska favours the development of these facilities and may be willing to arrange financing for their development, there can be no assurance that these infrastructure facilities can be developed on a timely and cost-effective basis. Energy risks include the potential for significant increases in the cost of fuel and electricity. The Preliminary Assessment assumes specified, long-term prices levels for gold, copper, silver and molybdenum. Prices for these commodities are historically volatile, and Northern Dynasty has no control of or influence on those prices, all of which are determined in international markets. There can be no assurance that the prices of these commodities will continue at current levels or that they will not decline below the prices assumed in the Preliminary Assessment. Prices for gold, copper, silver, and molybdenum have been below the price ranges assumed in Preliminary Assessment at times during the past ten years, and for extended periods of time. The project will require major financing, probably a combination of debt and equity financing. Interest rates are at historically low levels. There can be no assurance that debt and/or equity financing will be available on acceptable terms. A significant increase in costs of capital could materially and adversely affect the value and feasibility of constructing the project. Other general risks include those ordinary to very large construction projects including the general uncertainties inherent in engineering and construction cost, the need to comply with generally increasing environmental obligations, and accommodation of local and community concerns. The Company is also subject to the specific risks inherent in the mining business, as well as general economic and business conditions. For more information on the Company, Investors should review the Company's annual Form 40-F filing with the United States Securities and Exchange Commission and its home jurisdiction filings that are available at www.sedar.com.

Information Concerning Estimates of Measured, Indicated and Inferred Resources

This news release uses the terms "measured resources", "indicated resources" and "inferred resources". Northern Dynasty Minerals Ltd. advises investors that although these terms are recognized and required by Canadian regulations (under National Instrument 43-101 Standards of Disclosure for Mineral Projects), the U.S. Securities and Exchange Commission does not recognize them. Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. In addition, "inferred resources" have a great amount of uncertainty as to their existence, and economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, or economic studies except for Preliminary Assessment as defined under 43-101. Investors are cautioned not to assume that part or all of an inferred resource exists, or is economically or legally mineable.