Northern Dynasty Refutes Short Seller Claims

February 17, 2017

Short Seller's Report Based on Misstatements, Inaccuracies and "Anonymous Sources"

Northern Dynasty's Pebble Project Has Been Assessed by Independent Experts as a Globally Important Copper/Gold Asset with Multiple Development Options for Commercial Success

February 17, 2017, Vancouver, BC - Northern Dynasty Minerals Ltd. (TSX: NDM; NYSE MKT: NAK) ("Northern Dynasty" or the "Company") today responded to misleading criticism of its Pebble copper and gold project in the February 14, 2017 report by Kerrisdale Capital Management LLC ("Kerrisdale" or the "Short Seller1").

The Company and its board have evaluated each of the Short Seller's claims and believe they are unfounded, contain numerous errors and unsupported speculation and demonstrate a lack of understanding of the Company's business. The Company will consider and vigorously pursue any and all actions and remedies available to it to protect the interest of its shareholders.

Summarizing the Short Seller's Claims

The Short Seller, Kerrisdale, would apparently have you believe that Pebble, as one of the world's largest deposits of copper and gold, is worthless despite the fact that mining companies are profitably mining lower grade ore within a few hundred miles of it as well as at other operations around the world. The Short Seller would apparently have you believe that Anglo American, a major mining company which spent some US$600 million on Pebble, but was ultimately unwilling to spend the full $1.5 billion required to earn a 50% interest in Pebble, thinks the project is "worthless". The Short Seller would apparently have you believe that Pebble's challenges from the US Environmental Protection Agency ("EPA") are deserved, or that it is the first mining project to face regulatory challenges, despite what has been described by the Wall Street Journal as the EPA's regulatory "lawlessness" which they based on "sham" science (January 23, 2017, WSJ). The Short Seller would apparently have you rely on anonymous hearsay, supposedly from employees of Anglo American, who are making comments at odds with the public statements of the major mining company's own senior executives.

Investors who read the Short Seller's report should consider the following:

- Kerrisdale stands to realize significant gains in the event that the price of the Company’s stock declines.

- Kerrisdale is not a mining company and does not disclose any record of success in mining investments or issuing mining valuation or investment reports. On the contrary, Kerrisdale has a track record of aggressive short selling and activism. In contrast, Northern Dynasty’s Pebble team has extensive experience in mining and a formidable track record of success in developing and operating mines internationally.

- Kerrisdale relies on anonymous co-authors whose mining credentials, if any, Kerrisdale has not disclosed and who likewise may hold or have held short positions in Northern Dynasty. Specifically, Kerrisdale has not disclosed if these anonymous authors have any requisite technical qualifications or practical mining experience to substantiate the claims of the short report. In contrast, Northern Dynasty publicly files technical reports which have been certified by named, independent, experienced and reputable Qualified Persons (as defined by securities laws) who have certified the accuracy and completeness of these reports. An internationally recognized engineering firm conducted and compiled an extensive and independent Preliminary Assessment (also referred to as a Preliminary Economic Assessment, or “PEA”) of the Pebble Project on behalf of Northern Dynasty. This PEA, published in 2011, showed the project possesses significant value. While the analyses of this assessment now require updating, it remains a source of much useful information and is available for download at www.sedar.com. The PEA shows the large mineral endowment and potential of the Pebble Project.

- Kerrisdale’s short report purports to develop a zero value thesis without requesting or having had access to the necessary and extensive technical, analytical, geological and economic information that Northern Dynasty’s Qualified Persons used. No Kerrisdale personnel have visited the Pebble Project or had discussions with Northern Dynasty’s technical team or executives.

- Kerrisdale is apparently a troubled organization, which has recently been in the news for major client and staff defections and alleged senior staff personal misconduct.

Consider the Reaction to the Short Seller's Report by Independent Analysts 2:

From TD Securities:

Following the election of President Trump, [NDM] shares have outperformed the broader base metal market on the view that the EPA will withdraw its preemptive objections to Pebble, allowing the project to go through the formal NEPA permitting process. It is important to note that even prior to Trump's election, the company had announced planned mediation discussions with the EPA to resolve its dispute over the FACA case. Our view is that EPA will withdraw its objections, allowing the project to proceed to permitting by late-2017 or early-2018.

In terms of the project economics, the Short Seller's report cites that work completed by Anglo American and third-party engineers indicated that the upfront capital cost of Pebble would be roughly US$11-13bln. Importantly, no context around the project's size and scale was provided with the estimate, which we view as misleading. The estimate compares with the US$4.7bln in upfront capex outlined in Pebble's 2011 PEA for a 200,000tpd operation. We assume US$6.5bln of capex, with a 10%NAV estimate of US$1.24bln.

Assuming a resolution with the EPA in H1/17, the next critical step, in our view, will be the re-establishment of a partnership, which management is confident can be achieved this year. We expect the establishment of a partnership to be followed by the publication of a PFS, which could target a smaller higher-grade mine development scenario reducing both the capex and permitting objections.

We maintain our C$5.00 target price and upgrade our rating to SPECULATIVE BUY from Hold to reflect our return-to-target of 49%.

- Craig Hutchison, P. Eng, TD Securities Inc. February 16, 2017

From Stansberry's Investment Advisory:

Kerrisdale offered no new technical or scientific evidence. On the call, they labeled themselves as market generalists with no background in the mining industry. They made vague references to engineers, but would not disclose their names or credentials.

One of their main arguments is that mining giant Anglo American and other large miners walked away from the project because Northern Dynasty's resource is worth nothing. We disagree.

We think investors should be very skeptical of investment research that's published by any entity whose business depends on promoting a position (long or short) after establishing one -- whether it's a hedge fund manager with a history of drug abuse or an established industry titan. The fact is that having a bunch of money on the line (like Bill Ackman with Herbalife) tends to warp investors' judgement.

- Stansberry's Investment Advisory. February 2017

From Very Independent Research:

The short seller report was neither a mining technical report nor very much new.

- John Tumazos Very Independent Research, LLC. February 15, 2017

SETTING THE RECORD STRAIGHT

Pebble is One of the World's Largest Undeveloped Copper and Gold Resources

The Company will continue this discussion by reconfirming that the Pebble Project is one of the world's most important mineral resources, when measured by aggregate contained metals. The current estimate of these mineral resources at a 0.30% copper equivalent (CuEQ)3 cut-off grade comprise:

- 6.44 billion tonnes in the combined Measured and Indicated categories5 at a grade of 0.40% copper, 0.34 g/t gold, 240 ppm molybdenum and 1.66 g/t silver, containing 57 billion pounds of copper, 70 million ounces of gold, 3.4 billion pounds of molybdenum and 344 million ounces of silver; and

- 4.46 billion tonnes in the Inferred category at a grade of 0.25% copper, 0.26 g/t gold, 222 ppm molybdenum and 1.19 g/t silver, containing 24.5 billion pounds of copper, 37 million ounces of gold, 2.2 billion pounds of molybdenum and 170 million ounces of silver.

How does this compare to other similar assets?

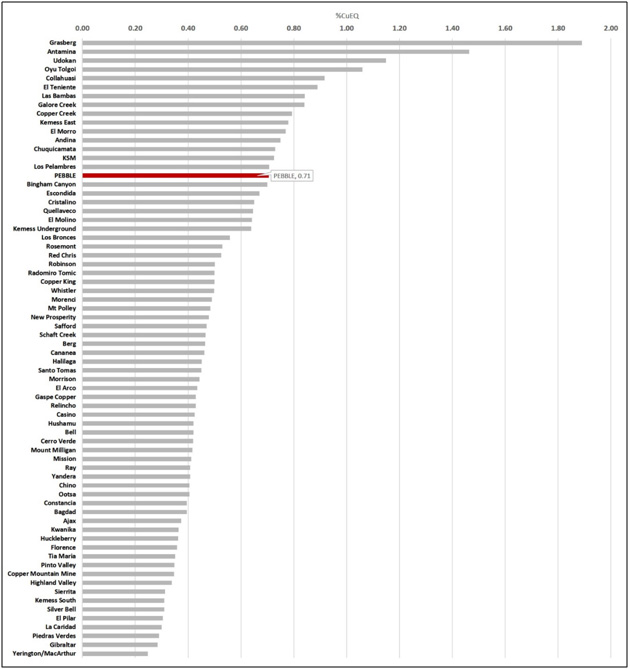

The Short Seller's contention that Pebble is a "low grade" deposit is not supported by the data. Pebble has an average CuEQ grade of 0.71%. The following graph shows Pebble in comparison to other major producing and non-producing copper projects. It shows that Pebble is in the top quartile of these deposits when ranked based on CuEQ grade.4

Comparison of Grades (% CuEQ) of Copper Deposits

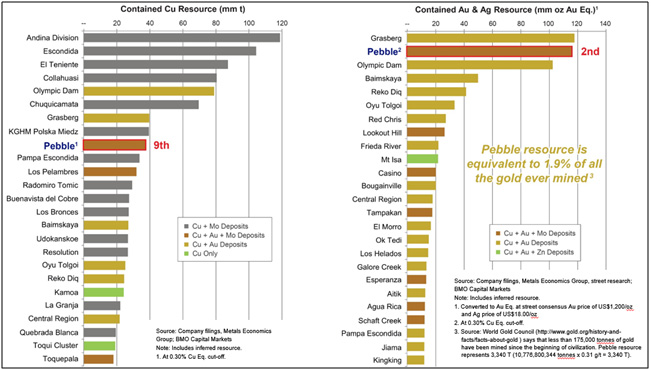

Further, the sheer scale of this immense copper/gold asset has attracted major mining company interest and continues to do so. Pebble is the world's largest undeveloped copper and gold resource in terms of contained metal. The deposit hosts the 9th largest copper resource and the 2nd largest gold resource in the world, as shown in the graphs below. The contained metal of this one deposit matches the reported reserves of many of the largest mining companies in the world. Bringing Pebble into production will be transformative for its shareholders.

Mine Planning and Economic Assessment

Like many large mining projects, the Pebble Project has had various owners, partners and major investors over the years such as Teck Resources, which owned Pebble before the big exploration successes at Pebble in 2004 to 2007 massively expanded the resource. Teck Resources continues to hold a royalty interest in part of the deposit after its 2002 sale of Pebble. With each such party came different priorities and interests, including with respect to mine development, timelines, scale and approach. What has never been denied is the potential and quality of this unique asset, nor Northern Dynasty's full commitment to work with interested parties to develop it.

Northern Dynasty's 2011 PEA demonstrated based on certain assumed mining design parameters (mine plan, mill through put etc.) that Pebble has a potential net present value measured in the billions of dollars and a mine life of 40 to 80 years. This long-lived mining project did not even deplete the full Pebble resource. The PEA was prepared by Wardrop Engineering Inc., now an affiliate of Tetra Tech Inc., an internationally recognized engineering group. The PEA showed that the commercial potential of a mine at Pebble is good at many commodity price and cost assumptions. Like all resource extraction projects, commercial viability is largely dependent on the outlook for the price of the commodity. This is especially true where the outlook has to span a period measured in decades due to the immense size of the mineral deposit. Northern Dynasty believes in the long-term demand for copper and gold and is highly confident that Pebble's viability will be demonstrated when it files the final mine design (as it evolves through the iterative permitting process) after the permitting process has been completed.

Contrary to the Short Seller's report, no mine planning scenario with a US$13 billion capital estimate was ever finalized, approved or adopted by Northern Dynasty or Anglo American as its 50% partner in the Pebble Limited Partnership ("Pebble Partnership"). In fact, Pebble Partnership staff, led by secondees from Anglo American, recognized the flaws with this work and continued studying development alternatives. Further, a review of a preliminary draft US$13 billion mine planning scenario by an independent engineering firm commissioned by Northern Dynasty identified issues with that study and identified savings that reduced the preliminary capital estimate by US$4 billion. As is well-understood by those with technical knowledge of the industry, there are a large amount of analyses conducted on very different assumptions of mine scale and costs to test development scenarios. The conclusions to be drawn from such work are used to inform mine planning and design and such work is not intended to represent the "most likely outcome" case for a mine. It is important to note that the Pebble Partnership has considered hundreds of preliminary mine design scenarios with different design components, operating parameters and scales.

The 2011 PEA is the only formal published report of the Pebble Project which assesses economics at a preliminary level.

The 2011 PEA was based on an internal Pebble Partnership study, known as the 2010 Value Seeking Phase study ("VSP") that used similar mining parameters as the PEA. The PEA projected Pebble to have significant asset value. Based on the development alternatives identified in that study, Anglo American, following completion of the VSP, continued to invest some US$320 million between 2010 and 2013 in Pebble until its withdrawal from the project in 2013.

Anglo American's Termination

During the 2013 mining downturn, Anglo American announced that it was reconsidering its development project pipeline in light of market conditions and was unwilling to invest another $900 million to earn a 50% interest in the Pebble Project and therefore terminated its earn-in option. At the time, Anglo American faced well-known capital constraints as a result of the commodity downturn and negative capital market conditions. In regards to that termination, newly appointed CEO Mark Cutifani cited a need to manage capital investment on its pipeline of long dated projects, while publicly referring to Pebble as "a deposit of rare magnitude and quality".

Even after its decision to withdraw from the project, Anglo American maintained a positive outlook on Pebble. "Our views on Pebble as a mining project are unchanged. ... We wish the project well, and express our thanks to those who have supported Pebble.... our decision to withdraw from the project is the result of an internal prioritisation of the many projects that we have in our portfolio," Anglo American spokesperson James Wyatt-Tilby told Bloomberg on September 30, 2013.

The Short Seller also claims that the Pebble Project was "pushing the boundaries" of engineering. That is simply untrue.

While the scale of Pebble engenders a significant, multi-component project, the scale and the engineering concepts incorporated in its development are not unique and are based on multiple similar mine developments around the world. Pebble sits at approximately 1,000 feet above sea level in rolling terrain, 60 miles from tide water that is ice-free 11 months of the year. After more than a decade of detailed investigation and analysis, no critical engineering issues have been identified with mine development, ore processing, and infrastructure. Thus, in fact, the conditions at Pebble are far less challenging than that faced by mines successfully developed in South America (high elevations, precipitous valleys, limited water supply), the Canadian Arctic (temperature extremes and severe logistical challenges), southeast Asia (massive precipitation and excess water balance conditions), and in northwest Alaska (permafrost, logistics challenges due to short shipping seasons and temperature extremes). The 2011 PEA work was based on customary and proven mining technologies.

Permitting the Pebble Project

Every mining project has opponents. However, Pebble enjoys considerable support for its efforts to advance the Pebble Project in Alaska today, including among elected officials, business interests, and regional and Alaska Native communities. The Short Seller tries to focus attention on the project's opponents while deliberately neglecting to mention the significant support the Pebble Project has had in Alaska, including opposition to what has been widely regarded as unfair efforts by the EPA to stall the project. Importantly, the State of Alaska was a co-plaintiff in PLP's 'statutory authority' case against the EPA.

Permitting and developing Pebble will be a multi-year process with multi-decade or multi-generational payoff. We are entirely committed to advancing the political and public consensus necessary to support a positive permitting outcome. The Company is advancing a comprehensive strategy to address EPA actions and stakeholder concerns through potential changes in project design, enhancing strategic partnerships with key constituencies and ensuring the project delivers significant benefits to the people of Bristol Bay and Alaska. What is absolutely clear is that many Alaskans are concerned about the EPA's pre-emptive actions, and they want the project to be fully but fairly evaluated through a comprehensive federal/state permitting process under the US National Environmental Policy Act ("NEPA").

The Company believes it will have the opportunity to appropriately respond to concerns raised by regulators, and to demonstrate that its final design will satisfy all federal and state environmental regulations and permitting requirements.

The EPA

Northern Dynasty and its technical advisors will provide full support to the lead federal regulatory agency to ensure that the Environmental Impact Statement ("EIS") completed at Pebble will be a rigorous scientific assessment of the environmental impact of a mine design that will incorporate robust engineering and environmental approaches and technologies. This will clearly demonstrate to the agencies and stakeholders that Pebble meets and exceeds all relevant federal and state environmental standards.

The Short Seller has no basis to predict that any future Democrat administration would seek to veto the Pebble Project, before or after the Pebble Project has received a positive Record of Decision following a comprehensive EIS process.

Northern Dynasty's financial position

Northern Dynasty is in a strong financial position having recently completed a C$47 million oversubscribed bought deal financing, contrary to the claim by the Short Seller.

The Company believes that its Pebble Project has a high likelihood of success. The Company further believes the Short Seller report is misleading as it contains numerous misstatements, comments attributed to "anonymous sources" and deliberate inaccuracies. It demonstrates that the Short Seller has no understanding of or experience in the mining industry or the development process of a mining project.

As typically results after a short report, various law firms have announced investigations into, or lawsuits against, Northern Dynasty. Management believes any such suits will prove equally baseless and they will be vigorously defended against.

Endnotes

- Short selling is the practice of selling borrowed shares and subsequently repurchasing them. In the event of an interim price decline, the short seller will profit, since the cost of repurchase will be less than the proceeds which were received upon the initial short sale.

- Permission to quote from the reports was neither sought nor obtained. The Company does not necessarily adopt the statements and opinions set forth by the analysts, and investors should review all information available to them.

- Copper equivalent (CuEQ) calculations use metal prices of US$1.85/lb for copper (Cu), US$902/oz for gold (Au) and US$12.50/lb for molybdenum (Mo), and recoveries of 85% for Cu, 69.6% for Au, and 77.8% for Mo in the Pebble West zone and 89.3% for Cu, 76.8% for Au, 83.7% for Mo in the Pebble East zone. Contained metal calculations are based on 100% recoveries. The estimate includes 527 million tonnes of Measured resources grading 0.33% Cu, 0.35 g/t Au, 178 ppm Mo and 1.66 g/t Ag and 5.9 billion tonnes of Indicated resources grading 0.41% Cu, 0.34 g/t Au, 245 ppm Mo and 1.66 g/t Ag. David Gaunt, PGeo., a Qualified Person who is not independent of Northern Dynasty is responsible for the estimate. For further details see the December 2014 Technical Report which is available at www.sedar.com.

- Resource and reserve data informing this chart, which is for illustrative purposes only, is based on public and third party sources believed to be accurate but this cannot be warranted, and it may contain information which in some cases may be several years old. Where available, proven and probable reserve grades have been used to calculate copper equivalence values. For those projects which have not declared a reserve, measured and indicated grades have been employed. Copper equivalence has been calculated by summing the revenue for all payable metals and dividing this figure by the revenue of 1% copper. Commodity prices used in this calculation are: Cu = 2.88/lb, Au = 1200/oz, Ag = 18/oz, Mo = 10/lb (all prices in US$).

- Notes on Mineral Terminology: Mineral Resources and Reserves are defined terms derived from Canadian Institute of Mining definitions. Similar terminologies are in use in elsewhere and are being considered for adoption in the United States. Mineral resources do not have demonstrated economic viability, but have reasonable prospects for eventual economic extraction. They fall into three categories: measured, indicated and inferred. Measured and indicated mineral resources can be estimated with sufficient confidence to allow the appropriate application of technical, economic, marketing, legal, environmental, social and governmental factors to support evaluation of the economic viability of the deposit. For measured resources: we can confirm both geological and grade continuity to support detailed mine planning. For indicated resources: we can reasonably assume geological and grade continuity to support mine planning. Mineral reserves are the economically mineable part of measured and/or indicated mineral resources demonstrated by at least a preliminary feasibility study. The reference point at which mineral reserves are defined is the point where the ore is delivered to the processing plant. Mineral reserves fall into two categories: a) proven reserves: the economically mineable part of a measured resource for which at least a preliminary feasibility study demonstrates that economic extraction is justified; and b) probable reserves: the economically mineable part of a measured and/or indicated resource for which at least a preliminary feasibility study demonstrates that economic extraction is justified. Northern Dynasty does not classify any of its mineralized material as reserves at this time. United States investors are advised that while “Measured” and “Indicated” resources are recognized and required by Canada and other countries, the United States Securities and Exchange Commission does not recognize them. United States investors are cautioned not to assume that all or any part of Measured or Indicated Mineral Resources will ever be converted into Mineral Reserves.

Qualified Persons

Stephen Hodgson, P.Eng., is an executive of Northern Dynasty and the Qualified Person who assumes responsibility for the scientific and technical discussion in this document.

About Northern Dynasty Minerals Ltd.

Northern Dynasty is a mineral exploration and development company based in Vancouver, Canada. Northern Dynasty's principal asset is the Pebble Project in southwest Alaska, USA, an initiative to develop one of the world's most important mineral resources.

For further details on Northern Dynasty and the Pebble Project, please visit the Company's website at www.northerndynasty.com or contact Investor services at (604) 684-6365 or within North America at 1-800-667-2114. Review Canadian public filings at www.sedar.com and U.S. public filings at www.sec.gov.

On behalf of the Board of Northern Dynasty Minerals Ltd.

Ronald W. Thiessen

President & CEO

Canadian Media Contact:

Ian Hamilton

DFH Public Affairs

(416) 206-0118 x.222

US Media Contact:

Dan Gagnier

Gagnier Communications

(646) 569-5897

Forward Looking Information and other Cautionary Factors

This disclosure document contains "forward-looking information" within the meaning of applicable Canadian securities legislation, and "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995 (collectively referred to as "forward-looking information"). The use of any of the words "expect", "plan", "update" and similar expressions are intended to identify forward-looking information or statements. These statements include expectations about the size, nature and/or ultimate economics of the Pebble Project, the success of the Company's multi-dimensional strategy to address the pre-emptive action of the EPA, the ability of the Company to proceed with permit applications for the development of the Pebble Project and the ability of the Company to obtain the necessary federal and state permits for the development of the Pebble Project. Though the Company believes the expectations expressed in its forward-looking statements are based on reasonable assumptions, such statements are subject to future events and third party discretion such as regulatory approval. For more information on the Company, and the risks and uncertainties connected with its business, Investors should review the Company's home jurisdiction filings at www.sedar.com and its filings with the United States Securities and Exchange Commission at www.sec.gov.

No securities regulatory authority assumes any responsibility for the contents of this disclosure.